Q1 2026 Container Market Analysis

The following Q1 2026 Container Market Analysis report, was conducted by Dr. Michael Tsatsaronis, Assistant Professor at the Department of Port Management and Shipping, National and Kapodistrian University of Athens, and his research team.

CONTAINER MARKET

The first quarter of 2026 presented a highly dynamic and fluctuating environment for the global containership market. The quarter commenced in January on a relatively positive and stable footing, supported by constrained capacity and high fleet utilization.

However, the landscape quickly shifted into a downward trend during February, heavily influenced by traditional seasonal lulls associated with the Chinese New Year and a corresponding reduction in industrial activity.

By March, the market was engulfed in heightened uncertainty due to escalating geopolitical tensions in the Middle East, maritime transport disruptions, and rising energy costs, resulting in a notably cautious medium-term outlook. Despite the volatility in the freight market, shipowners continued to strategically invest in fleet renewal, prioritizing environmentally compliant, dual-fuel newbuildings to adapt to shifting trade routes and future disruptions.

Meanwhile, the demolition sector, which began the year in a stagnant state, slowly awakened as the quarter progressed, driven by the pressure of massive newbuilding deliveries and the looming enforcement of stricter carbon standards.

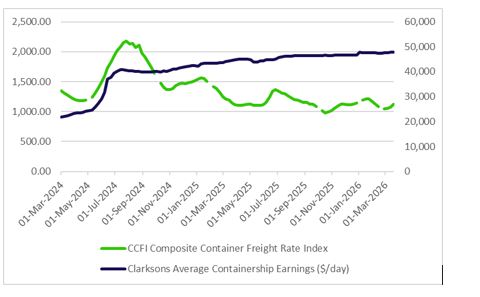

FREIGHT MARKET

The containership freight market experienced significant volatility and varying pressures throughout the first quarter. During January, the market demonstrated clear signs of measured strengthening.

The broader conditions remained highly supportive of operators, even though there was an absence of a clear and unified market direction. Freight rates were successfully maintained at stable levels, an achievement directly attributed to high fleet utilization and notably limited levels of idling.

Furthermore, constrained capacity availability across certain vessel sizes acted as a crucial stabilizing factor. Despite these positive indicators, market performance was not uniform across all trade lanes, with noticeable variations observed in fundamental demand dynamics and charter duration lengths.

Within this complex environment, market participants kept their activity highly selective, focusing intensely on risk management and the preservation of operational flexibility.

Overall, January reflected a market operating on a positive footing but plagued by limited visibility, with rates influenced simultaneously by supportive fundamentals and ongoing macroeconomic uncertainties.

Transitioning into February, the containership freight market experienced a distinct downward trend. Weekly data consistently indicated successive declines in overall freight rates. This negative development was primarily associated with fundamentally weaker demand during the period surrounding the Chinese New Year holidays.

During this time, industrial and manufacturing activity in China was temporarily reduced, severely impacting export volumes. Consequently, the market presented a significantly more subdued outlook. The underlying demand for maritime transport appeared visibly lower, directly causing freight rates to move and settle at reduced levels.

Table 3: Containers Freight Market Analytics

| Clarksons Average Containership Earnings ($/day) | CCFI Composite Container Freight Rate Index | |

| 2 years average | 41126.05 | 1365.90 |

| 1 year average | 45956.38 | 1154.84 |

| Quarter average | 47208.62 | 1147.78 |

| % Annual Change | 9% | -100% |

| Quarter Volatility | 490.13 | 42.37 |

| Annual Max | 47713.72 | 1369.34 |

| Annual Min | 43668.20 | 973.13 |

| Quarter Max | 47713.72 | 1209.85 |

| Quarter Min | 46621.35 | 1088.14 |

By March, the narrative of the freight market was completely characterized by increased global uncertainty. The market operated under the heavy impact of intense developments and conflicts in the Middle East.

Reduced capacity availability became a prominent issue due to severe disruptions in global maritime transport, which subsequently created immense operational pressures on the market. Furthermore, rising energy costs began to negatively affect the broader economic environment.

Concurrently, weaker global demand paired with lower expected growth in overall container trade contributed to a much more cautious market outlook. Because of these combined negative factors, the market’s prospects remained highly uncertain in the medium term.

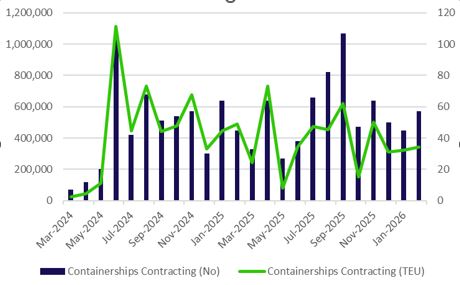

NEWBUILDING – SALES & PURCHASE

Investment in new vessels remained robust as operators looked to secure future capacity. In the previous year, the surge in orders for new container ships was predominantly driven by companies needing to radically renew their aging fleets, strictly comply with new environmental regulations, and rapidly adapt to structural changes in global shipping routes.

The market was fully expected to continue at this exact same aggressive pace into 2026. This projection proved accurate in January, which recorded fresh orders for a total of 16 new ships, while the prominent operator Evergreen notably ordered 23 new vessels directly from a Chinese shipyard.

Despite the industry facing a huge number of TEUs scheduled to be delivered within the year, shipping companies actively continued to invest heavily in shipbuilding to effectively cope with future geopolitical and economic disruptions.

In February, overall ordering activity continued, albeit at a noticeably slower pace compared to the previous month. A major highlight was Maersk placing a significant order for eight large dual-fuel containerships, a move that heavily reinforced the industry’s strategic shift toward strict environmental regulatory compliance.

In parallel, market reports strongly highlighted that the recent massive surge in containership orders had successfully led to historically high TEU levels within the global orderbook. Furthermore, the average size of vessels specifically scheduled to operate on the major East-West routes continued to aggressively increase, accurately reflecting the ongoing and dominant trend toward deploying significantly larger ships.

March was heavily marked by escalating geopolitical tensions in the Middle East, a situation that created even greater uncertainty for the shipping market. Nevertheless, new containership orders bravely continued.

The indefinite avoidance of the critical Strait of Hormuz by major shipping companies is fully expected to absorb any excess fleet capacity due to the necessity of rerouted, significantly longer voyages traveling via the Cape of Good Hope.

During this tense period, Euroseas Ltd. specifically ordered two new, highly specialized 2,800 TEU high-reefer containerships from the Huanghai Shipbuilding Co., Ltd. shipyards located in China. Additionally, Yang Ming successfully ordered six newbuilding containerships, each boasting a massive carrying capacity of 13,000 TEU.

These specific newly ordered ships will feature advanced dual-fuel and LNG capabilities. Analysts project that significantly more orders will be finalized and announced by major companies in the upcoming few months.

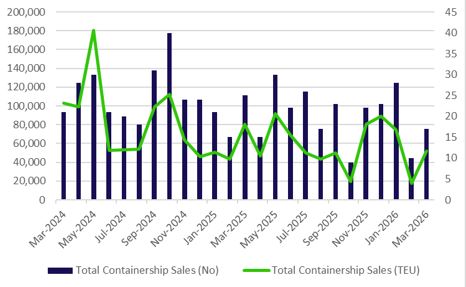

The Sale and Purchase (S&P) sector for containerships exhibited varied momentum. The year commenced with strong indicators in January, reflecting a rising demand for containerships. BF Shipmanagement completed the purchase of a 2023-built Neo-Panamax vessel, boasting a capacity of around 13,000 TEU, from its previous owner, Capital Clean Energy Carriers (CCEC).

Furthermore, the Tsakos Group successfully acquired a second-hand Panamax vessel, featuring a capacity of approximately 4,500 TEU and built in 2010, from Atlantica Shipping. These high-profile purchases successfully indicated a strong start for the second-hand containership market in 2026.

Activity persisted into February, albeit on a slightly smaller scale, when Metrostar Management Corp officially acquired the vessel named Warnow Beluga. This specific vessel is a feeder ship that was originally built in 2008 and holds a total capacity of 1,300 TEU.

By March, however, there was a recorded low level of activity across the Sales & Purchase containership market. According to market sources, MSC purchased two Sub Panamax vessels.

Both of these acquired units were built in 2006, feature a capacity of 2,602 TEU, and cost the operator 25 Million USD each. Additionally, during this slow month, the vessel known as “Erasmus Oasis” was officially sold for 11 million USD to an undisclosed, unknown buyer. This specific vessel operates as a feedermax ship and has a listed capacity of 1,049 TEU.

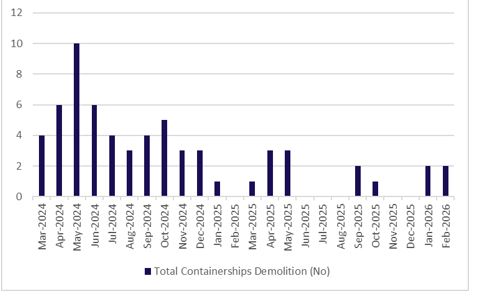

DEMOLITIONS

Demolition of containerships has dropped globally to historic lows in 2025: only eight to ten containerships have been scrapped so far this year, compared with 81–82 units in 2023. Simultaneously, BIMCO estimates that at least 500 containerships (≈ 1.8 million TEU) globally are overdue for recycling—the highest backlog since the 1970s.

By 2025 a quarter of the global containership fleet exceeds 20 years old. Such a sharp drop in containership scrapping despite an aging fleet and record backlog suggests that many older ships will remain in service for the foreseeable future.

Unless demolitions rise dramatically in 2026, the overhang of obsolete capacity risks contributing to oversupply, downward pressure on freight rates, and idle tonnage in the medium term, leading to serious market imbalance within 2027.

Greek shipping outlets echo that demolitions have nearly dried up, partly because owners are keeping older tonnage alive, helped by still-favorable freight income and high second-hand values.

However, if freight markets deteriorate or regulatory pressure increases (e.g., environmental rules), we could see a delayed but sharp wave of scrapping. Analysts argue that to offset the huge orderbook of newbuilds, the industry needs to scrap up to 4.5 million TEU by 2030, a level not seen in decades.

The market finally showed promising signs of awakening during February. Several aging units, most notably including the feeder vessel “Sunny Spruce”, finally withdrew from the active fleet for permanent recycling.

Completely overlooking the currently high charter rates, the undeniable mounting pressure of incoming newbuilding deliveries slowly but steadily began forcing older tonnage out of active service. Industry analysts firmly expect scrap prices to remain strong and firm at approximately $510/LDT, a price level heavily supported by an increasingly tightening supply of viable ships.

March subsequently witnessed a slight but notable uptick in ship recycling activity. Owners practically began offloading vintage maritime units, such as the vessel Kokopo Chief, as a strategic maneuver to carefully manage comprehensive fleet renewal.

While the broader demolition market remains incredibly tight due to persistent ongoing regional disruptions, scrap prices successfully stabilized at highly attractive financial levels. During March, these prices currently averaged $465/LDT within the shipyards of Bangladesh.

Expert industry sources strongly suggest that the potent combination of a massive global orderbook and the implementation of much stricter carbon emission standards will inevitably drive significantly more mid-sized tonnage directly toward the breakers by the end of the current year.

Written by Dr. Michael Tsatsaronis, Assistant Professor at the Department of Port Management and Shipping, National and Kapodistrian University of Athens, together with his research team: Zacharopoulou Efthimia, Vitzilaiou Anastasia, Skouli Maria Aikaterini, Foteinakis Nikolaos

The post Q1 2026 Container Market Analysis appeared first on Container News.

Content Original Link:

" target="_blank">