Bunker market stays volatile in Week 21

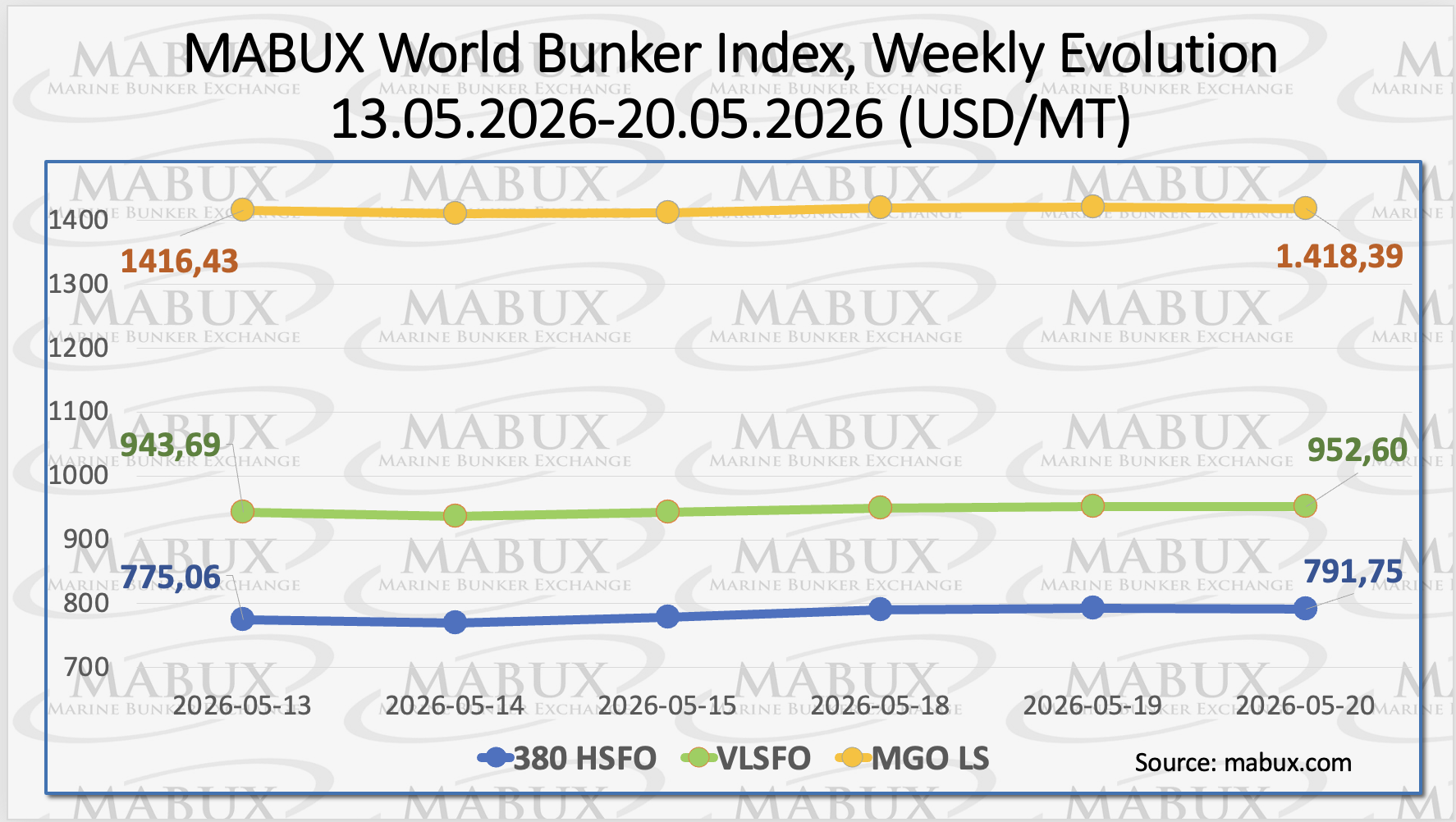

The global bunker market remained broadly stable during Week 21, with limited price fluctuations shaping overall market dynamics. The 380 HSFO index increased by US$16.69, rising from US$776.06/MT to US$791.75/MT and approaching the psychological US$800 mark once again.

The VLSFO index also moved higher, gaining US$8.91 week-on-week to US$952.60/MT, compared to US$943.69/MT the previous week. Meanwhile, the MGO LS index recorded a smaller increase of US$1.96, advancing from US$1,416.43/MT to US$1,418.39/MT. At the time of writing, the global bunker market continued to display mixed and irregular price movements, with no clear directional trend emerging.

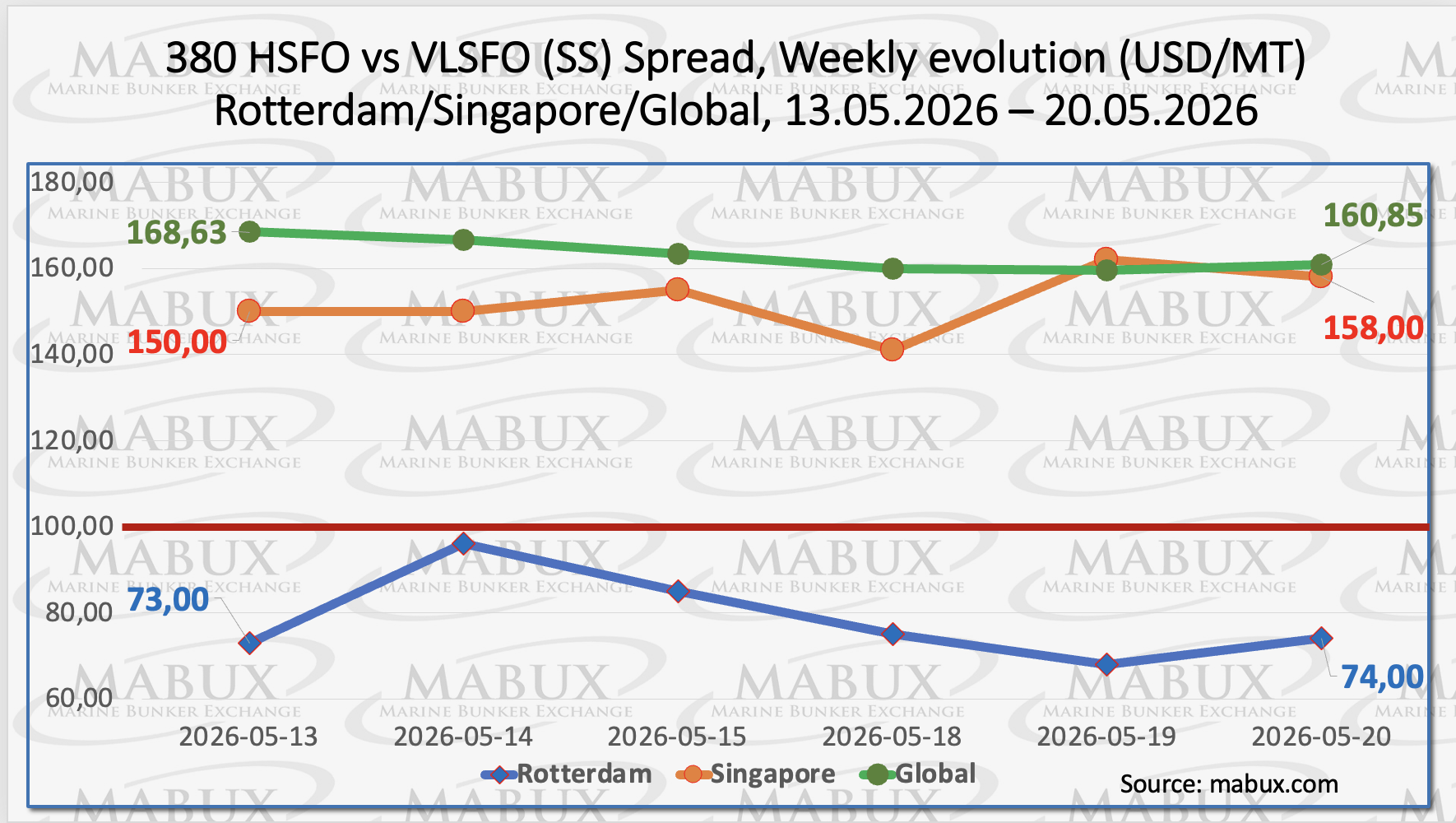

The MABUX Global Scrubber Spread (SS) — the price differential between 380 HSFO and VLSFO — narrowed by US$7.78 over the week, declining from US$168.63 to US$160.85. Despite the drop, the spread remained comfortably above the psychological US$100.00 breakeven threshold for scrubber economics. The weekly average of the index edged higher by US$2.08.

In Rotterdam, the SS Spread remained largely unchanged, increasing marginally by US$1.00 from US$73.00 to US$74.00, while the port’s weekly average spread declined by US$33.33. In Singapore, the 380 HSFO/VLSFO spread widened by US$8.00, rising from US$150.00 to US$158.00, while the weekly average in the port gained US$42.50.

Sergey Ivanov, Director of MABUX, said spread levels above US$100.00 continue to indicate stronger cost efficiency for scrubber-equipped vessels consuming 380 HSFO compared to vessels operating on conventional VLSFO. He added that mixed and irregular fluctuations in the SS Spread are likely to continue amid the current relative stability in the bunker market.

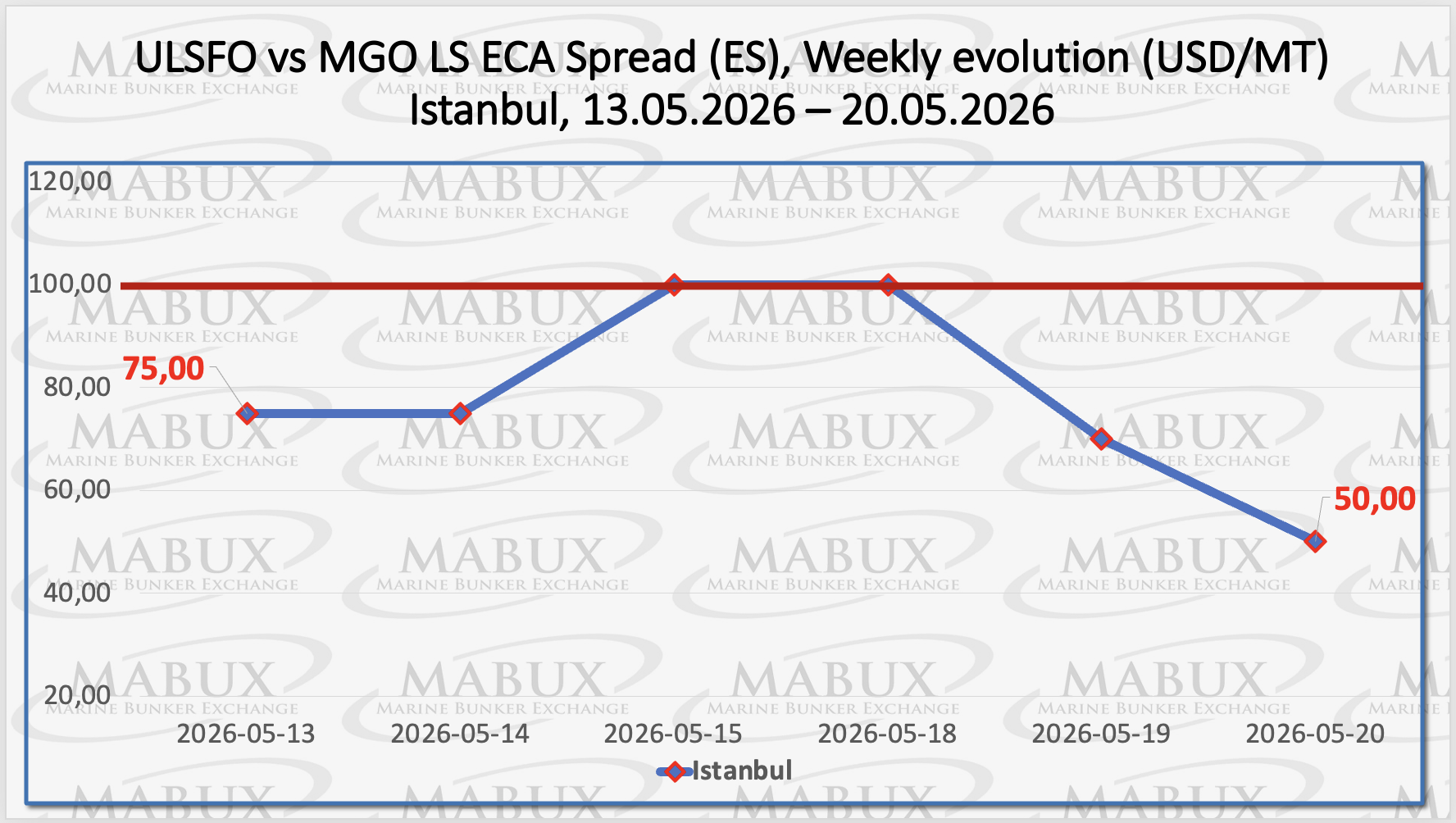

The Istanbul ECA Spread (ES) resumed its downward movement by the end of the week, declining by US$25.00 from US$75.00 to US$50.00 after briefly reaching the US$100.00 level during the reporting period. However, the weekly average of the index increased by US$17.50. The Venice ECA Spread remains suspended due to the lack of regular market quotations.

Ivanov commented that current ECA Spread levels remain well below the US$100.00 threshold, highlighting continued volatility and uneven pricing dynamics across the global bunker market. He expects the ECA Spread to undergo a moderate upward correction next week.

The Institute for Energy Economics and Financial Analysis (IEEFA) warned that the European Union’s dependence on U.S. LNG imports could rise sharply, potentially accounting for up to 80% of total EU LNG imports within the next two years. U.S. LNG already represents 58% of the bloc’s total LNG intake, raising concerns over supply security and overreliance on a single supplier. IEEFA urged the EU to accelerate investments in renewable energy and heat pumps to reduce gas demand.

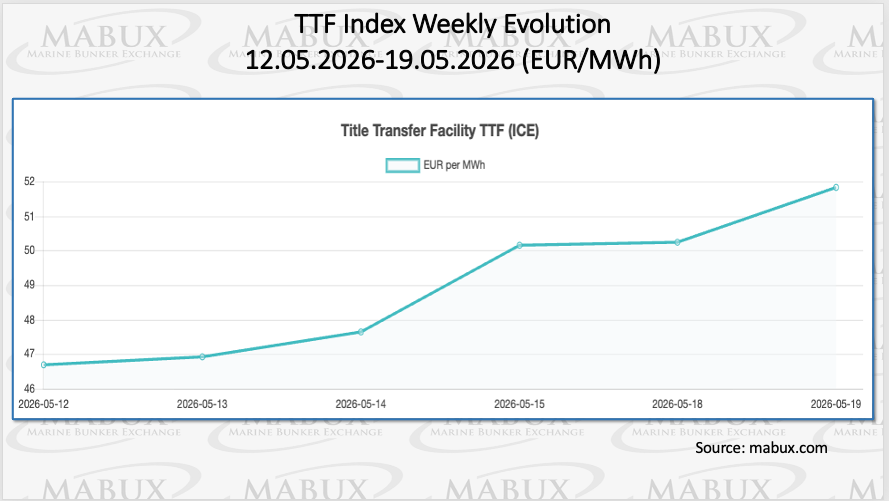

European underground gas storage levels continued to recover gradually as of May 19, reaching 36.67% of total capacity, up 1.10 percentage points week-on-week. However, storage levels remain 24.79% below the 61.46% recorded at the start of the year. Meanwhile, the European TTF gas benchmark rose by €5.132/MWh to €51.816/MWh, compared to €46.684/MWh the previous week.

The price of LNG as bunker fuel at the port of Sines, Portugal, increased sharply by US$150.00 to US$1,209/MT from US$1,059/MT the previous week. At the same time, the price spread between LNG and conventional fuel narrowed significantly to US$96 in favor of LNG, compared to US$220 a week earlier. On May 18, MGO LS was quoted at US$1,305/MT at the port of Sines.

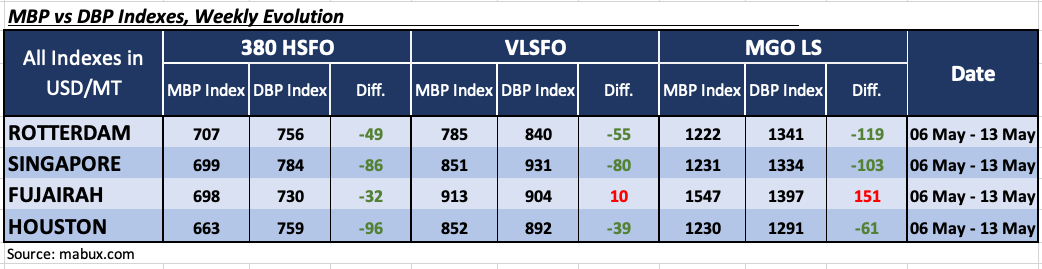

At the end of Week 21, the MABUX Market Differential Index (MDI) — which measures the ratio between market bunker prices (MBP) and the MABUX digital bunker benchmark (DBP) — showed mixed dynamics across Rotterdam, Singapore, Fujairah, and Houston.

In the 380 HSFO segment, Fujairah returned to the undervalued zone, resulting in all four major ports being assessed as undervalued. Discounts widened across all hubs, increasing by 7 points in Rotterdam, 34 points in Singapore, 33 points in Fujairah, and 50 points in Houston.

In the VLSFO segment, Fujairah remained the only overvalued port, although its premium narrowed by 26 points. Rotterdam, Singapore, and Houston continued to be undervalued. Discounts widened by 44 points in Rotterdam and 35 points in Houston, while Singapore recorded a marginal 5-point reduction in undervaluation.

In the MGO LS segment, Rotterdam, Singapore, and Houston all remained undervalued, while Fujairah continued to be the sole overvalued port in this category, with its premium increasing by 35 points.

Sergey Ivanov noted that the balance between overvalued and undervalued ports shifted slightly toward undervaluation during the week, mainly due to Fujairah returning to the undervalued zone in the 380 HSFO segment. He added that the broader DBP trend continues to show limited and mixed fluctuations, which are likely to persist next week.

Ivanov also said the bunker fuel market remains supported by elevated geopolitical risks that continue to underpin global oil prices. Additional pressure comes from concerns over potential shipping disruptions through the Strait of Hormuz and uncertainty surrounding alternative regional supply routes. According to Ivanov, global bunker indices are expected to continue moving in a volatile and irregular pattern, without establishing a sustained upward or downward trend. He warned that any escalation in the military confrontation between the United States and Iran could trigger another sharp spike in bunker prices.

Content Original Link:

" target="_blank">

Stock Forecasts")